Lesetid

5 min lesetid

Publisert

08. des. 2025

Artikkelen er flere år gammel

Credit markets update:

Nordic High Yield enters year-end after one of its most constructive periods to date.

Secondary markets have been resilient even during brief episodes of stress, credit losses have remained modest and elevated coupons have supported strong returns. The primary market has been the dominant story, with issuance approaching NOK300bn and pricing holding tight relative to historical medians. How did the market reach this point, and which shifts defined the year?

We are closing in on the end of what has been a remarkable year for Nordic HY. The secondary market has been highly constructive, and the brief period of turmoil in April demonstrated how increased market size has improved liquidity and depth.

As in other markets, Nordic HY traded down during that episode, but in contrast to earlier years, price discovery remained high, with multiple sellers and bidders active at the same time. This reflects not only a more diversified investor base, supported by a growing share of Non-Nordic investors, but also greater variation in investor strategies within the region.

While the episode was too short to fully stress-test the Nordic market, the signals we saw from the secondary market were highly encouraging.

While index spreads, now trading at 491bps, are 74bps higher than at the end of last year, most of this repricing stems from shifts in index constituents. The monthly index adjustments have contributed 56bps of widening, leaving only 18bps attributable to repricing of underlying bonds.

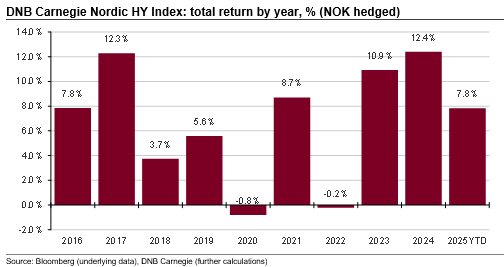

With a credit duration of around 2.4 years, that implies a credit loss of 45bps this year. This is modest relative to an average cash coupon of 8.4% in 2025. Index returns now stand at 7.8% YTD, broadly in line with our January expectation of 7-8% but slightly below our August estimate of 9%.

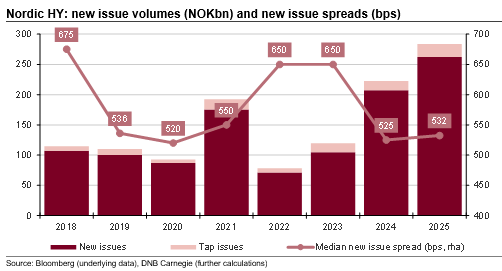

The real story this year has come from primary markets. 2024 had delivered record volumes, and few had expected anything close to that to repeat in 2025. My January projection was for new issue volumes to reach NOK170-200bn, but this was revised to NOK260-280bn in August.

As things stand now, new issue volumes are at NOK283bn, with a few weeks still left of the year. Excluding tap issues, the volume has reached NOK262bn, NOK55bn above last year.

Deal tally broadly unchanged. The number of new issues is similar to previous years, and both 2021 and 2018 recorded higher deal counts. The rise in volumes has therefore been driven by larger transactions rather than more issuers.

Record high average issue size. Excluding taps, the average new issue size reached NOK1400m, up from NOK1100m in 2024 and NOK700m on average in 2018 to 2023.

A shift in sector mix. E&P and oil service accounted for NOK45bn, down from NOK52bn last year. Consumer goods and services more than doubled to NOK47bn. TMT reached NOK35bn, while industrials totalled NOK32bn.

The year of sponsorship. Sponsor activity increased further, supported by demand from continental Europe. Volumes rose from NOK60bn in 2024 to NOK92bn this year, accounting for one third of total issuance.

Debut issuers even more active than before. First time issuers raised NOK140bn, an increase of NOK50bn from last year. Repeat issuers also expanded their activity, with volumes rising from NOK133bn to NOK143bn.

Non-Nordic firms remained active. Volumes increased slightly from NOK91bn to NOK95bn, maintaining a significant presence at around one third of the market.

FX issuance once again at the core of Nordic HY. 72% of new issue volumes came in USD or EUR. NOK accounted for 10% and SEK for 17%.

At this stage it is difficult to assess whether credit quality has shifted in a meaningful way. What we can observe is that all segments priced somewhat tighter than their median levels from previous years. Moreover, as discussed in our recent Nordic Credit Compass, there are also signs that recent cohorts are transitioning towards default at a slightly faster pace than before. Weaker credit quality is not necessarily a concern in itself, but it should be paired with tighter structures and a moderate widening in new issue spreads. At times the opposite appears to have been the case this year.

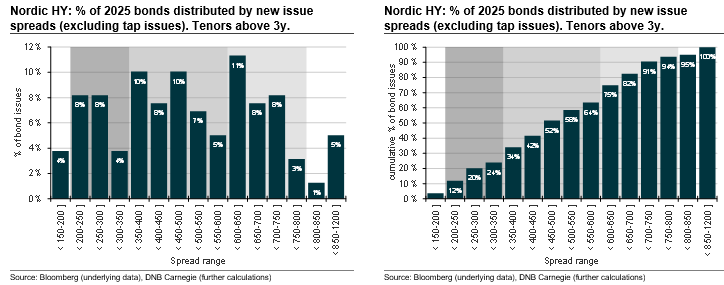

To illustrate current pricing dynamics, we have separated bond issues with tenors of at least three years by spread range. The distribution of spreads, and the corresponding cumulative distribution, reveal a clear drift towards the tighter end within each quality group.

A majority of issuers typically perceived as high-quality have priced between 200-300bps. Mid-quality names have typically priced in the ranges of 350-400bps or 450-500bps. Among the perceived higher-risk names, pricing has been concentrated between 600-650bps. These patterns should not be read as qualitative judgements on individual issuers. My intent is to illustrate, in broad terms, how the market has priced transactions this year. The buckets are visual tools, not statements about issuer quality, and individual names may not align perfectly with any one category.

One area where pricing has shifted most visibly is among sole mandates, which this year have been concentrated in EUR-denominated sponsor-backed deals by Non-Nordic issuers. As mentioned above, other segments have also priced tighter, although with less deviation from historical norms.

In summary, 2025 has been a year defined by strong secondary market performance, unusually resilient price discovery during brief periods of stress, and a primary market that has expanded in size, depth and diversity. Issuers have benefited from deeper and more diversified pools of capital, taking advantage of improved liquidity and richer pricing. The latter reflects the strength of demand, as more investors have gravitated towards the elevated credit returns of the Nordic market, supported by continued high risk-free rates and improved market liquidity.

This has been a deliberately backward-looking review. I will return with a full 2026 outlook in early January. My thoughts at this stage are that next year will likely continue the trends we have seen in 2025, with returns around 8% and further expansion of the Nordic market as more firms take advantage of the flexible platform and improved depth it offers.

Merk: Å kjøpe og selge aksjer innebærer høy risiko fordi verdien i verdipapirer vil svinge med tilbud og etterspørsel. Historisk avkastning i aksjemarkedet er aldri noen garanti for framtidig avkastning. Framtidig avkastning vil blant annet avhenge av markedsutvikling, aksjeselskapets utvikling, din egen dyktighet, kostnader for kjøp og salg, samt skattemessige forhold.

Innholdet i denne artikkelen er ment verken som investeringsråd eller anbefalinger. Har du noen spørsmål om investeringer, bør du kontakte en finansrådgiver som kjenner deg og din situasjon.