Publisert

09. mar. 2026

Artikkelen er flere år gammel

Credit markets update:

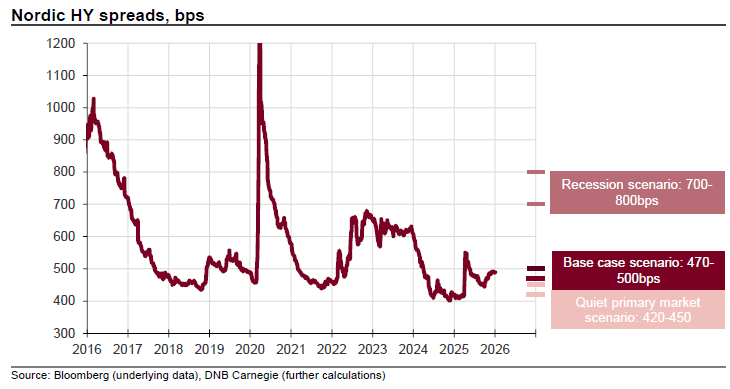

YTD returns in the Nordic HY market are 1.9% (NOK hedged). The average cash yield is 7.59% and the credit spread is 469bps.

Credit and interest rate duration stand at 2.37 and 0.96, respectively.

The month-end roll in late February mechanically tightened spreads by around 12bps. Even after adjusting for this effect, spreads ended the week roughly 3bps tighter than the week before. The move was largely driven by name-specific repricing in Shearwater, Norske Skog and Diversified.

Outside these names, the Norwegian market was broadly stable, with limited price movement apart from KD Pharma, which traded somewhat lower. In contrast, the Swedish market experienced higher volatility. Nearly half of SEK bonds priced down over the week, reflecting weaker sentiment and somewhat reduced liquidity amid the war in the Middle East. Swedish spreads widened by around 21bps over the week, although part of this move also reflects the month-end index roll.

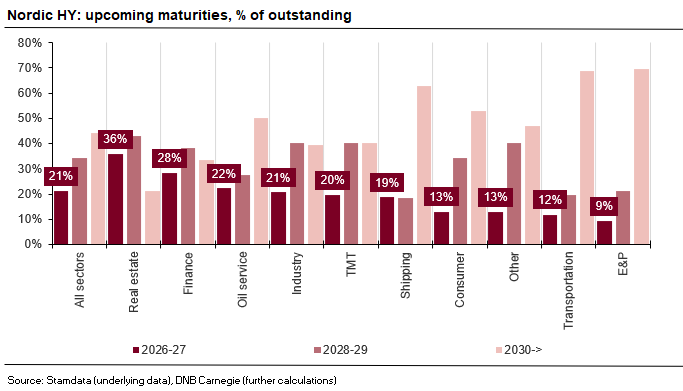

Following the recent moves in the oil price over the weekend, spreads may widen somewhat from current levels as markets begin to price a more stagflationary environment. That said, refinancing risks in the Nordic HY market remain limited. The maturity wall stands at just 7% in 2026 and 14% in 2027.

There are, however, clear sector differences. Real estate screens weakest from a refinancing perspective, with around 36% of outstanding volumes maturing in 2026-27. At the other end of the spectrum sits the E&P sector, where only around 9% of bonds mature over the same period.

The modest refinancing wall and the high carry offered by the market remain supportive features of Nordic HY. In addition, the floating-rate structure of most bonds means coupons would increase if risk-free rates move higher, providing some protection in a stagflationary environment. At the same time, the market is heavily exposed to cyclical industries, meaning that a global recession would likely weigh on earnings and increase default risk. As outlined in our January Outlook, such a scenario could push index spreads toward the 700-800bps range.

The situation nevertheless remains highly fluid and largely dependent on political developments, which are inherently difficult to forecast. Relatively speaking, the Nordic HY market continues to offer an attractive risk-reward profile in our view. However, Nordic spreads are unlikely to remain insulated if global risk assets reprice more meaningfully.

Merk: Å kjøpe og selge aksjer innebærer høy risiko fordi verdien i verdipapirer vil svinge med tilbud og etterspørsel. Historisk avkastning i aksjemarkedet er aldri noen garanti for framtidig avkastning. Framtidig avkastning vil blant annet avhenge av markedsutvikling, aksjeselskapets utvikling, din egen dyktighet, kostnader for kjøp og salg, samt skattemessige forhold.

Innholdet i denne artikkelen er ment verken som investeringsråd eller anbefalinger. Har du noen spørsmål om investeringer, bør du kontakte en finansrådgiver som kjenner deg og din situasjon.