Lesetid

6 min lesetid

Publisert

17. nov. 2025

Artikkelen er flere år gammel

Credit markets update:

Debt is the natural and economically efficient way to fund large infrastructure cycles.

Recent commentary about an AI bubble has raised concerns about debt-funded expansion, stock market concentration and the pace of technological development. Several of the claims touch directly on credit and capex dynamics and merit a closer look, particularly the interpretation of large investment figures and the recent widening in tech spreads.

I read an article in the Norwegian newspaper DN last week about an AI bubble and felt that several of the specific claims deserve clarification. I will leave the bubble debate aside and instead focus on the statements that are relevant for credit, capex and funding.

The article builds on a few key arguments: First, it suggests that Nvidia’s current dominance in equity markets relies on loss-making companies such as OpenAI that have not yet found a way to earn money. It then claims that “OpenAI plans to spend, that is borrow, USD1400bn in coming years at the same time as it is not earning money. It has come to the point where OpenAI has reached out to the US government for loan guarantees.”

The article also argues that OpenAI must be first: “If they are only two weeks behind their competitors, it will be worthless.” It then moves to the stock market, highlighting concentration risk by noting that a majority of the world’s ten largest companies are major technology firms.

Finally, it transitions to debt markets, claiming that “investors are starting to worry that interest expenses are rising too rapidly for tech companies” because of large debt-funded investments. The spread on tech company debt is said to have risen from 50 to 78 basis points, the highest since April this year.

Naturally, there is a lot to take in, including whether Nvidia truly relies on loss-making AI companies and whether OpenAI would be “worthless” if it fell two weeks behind competitors. I will leave those aside because it would be epistemic trespassing. Knowledge in one field does not translate automatically to another. My comments here relate solely to the credit, capex and funding aspects of the article.

This is not what the source actually says. Sam Altman’s statement refers to about 1.4 trillion dollars in data-centre commitments over the coming years. It is phrased as system-wide infrastructure investment, not as borrowing on OpenAI’s balance sheet. The figure reflects the long-term capital required across cloud providers, hardware suppliers, data-centre operators and sovereign investors. It is a mischaracterisation to present it as an OpenAI debt plan.

Loan guarantees are standard in large infrastructure cycles. The US government has used them for Intel’s semiconductor plants, Tesla’s early factory expansion, nuclear projects such as Vogtle and Hinkley Point, and a wide range of grid and energy investments. If anything, such guarantees reflect the strategic importance of the infrastructure rather than financial stress at the borrower level.

The proposed ‘Stargate’ project reinforces this point. It is conceived as a system-level data-centre build-out requiring coordinated investment by cloud providers, hardware suppliers and potentially public actors. Such projects are typically financed through a mix of corporate bonds, long-term contracts and, in some cases, loan guarantees, not through the balance sheet of any individual AI company.

The article frames debt-funded infrastructure as inherently negative. This is not supported by financial theory or historical precedent. In reality, debt is the natural and economically efficient way to fund large infrastructure cycles. There are several reasons for this:

1. Infrastructure produces long-duration, predictable cash flows

Once operational, assets like data centres, transmission lines, telecom networks and rail systems generate relatively stable revenues over many years. These match naturally with fixed coupon payments and long amortisation schedules. This cash-flow profile is fundamentally suited to bond markets.

2. Equity is too expensive and dilutive for large-scale build-outs

Infrastructure requires very high initial capex. Funding this with equity would result in:

- dilution of existing shareholders

- significantly higher financing costs (cost of equity often 10–15%)

- lower returns on invested capital

By contrast, investment-grade issuers can raise debt at spreads of 60–100bp over risk-free rates, with long maturities and predictable servicing.

3. Every major infrastructure cycle in modern history has been debt-funded

This is not unique to AI; it is the rule:

- Telecoms: mobile networks, fibre rollouts, switching centre

- Cloud computing: AWS, Azure and Google Cloud expanded almost entirely via recurring bond issuance and operating cash flow

- Electricity grids: transmission lines and generation capacity financed through multi-decade debt

- Railways: historically among the world’s largest bond issuers

- Semiconductor fabs: Intel, TSMC and Samsung rely heavily on debt financing, government support and long-term supply agreements

AI infrastructure, data centres, GPU clusters, cooling systems, grid connections, power capacity, belongs to the same category. These projects have long useful lives, high upfront costs and predictable utilisation curves once deployed.

4. Scale alone forces financing through the bond market

JPMorgan, Goldman Sachs and Morgan Stanley estimate that global AI infrastructure could require USD 2–6 trillion in cumulative investment over the next decade. No company can fund this with equity without massive dilution and depressed valuations. Bond markets exist to absorb this type of long-duration issuance at acceptable cost.

5. AI infrastructure resembles a utility in how it is financed

Even though the end-products are digital, the financial profile is closer to a digital utility: long-lived, high fixed cost, stable returns, and mission-critical for the economy. Utilities are financed primarily by the bond market. It is consistent that AI follows the same pattern.

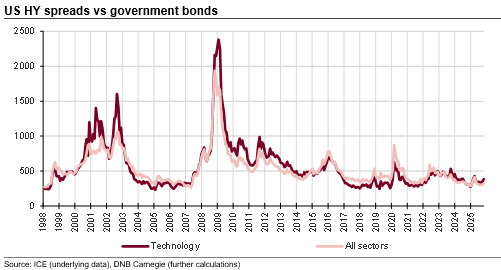

Borrowing costs for large technology issuers have risen, but not dramatically. In US high yield, tech spreads have widened from 300bps at the end of last year to 384bps at the end of last week. For comparison, broad-market spreads across all sectors have moved from 310bps to 324bps. There has therefore been a tech-specific adjustment, but spreads remain low by historical standards. The median spread since 1998 is 464bps for HY tech and 470bps for the broad market. By all measures, spreads remain rich, which is notable given the increase in tech-related supply we now see in bond markets.

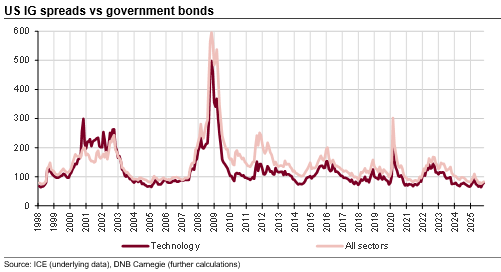

The picture is similar in investment grade. US tech spreads have risen from 66bps at the end of last year to 79bps last Friday. Broad-market spreads are broadly unchanged at 83bps. Historical medians are 102bps for tech and 129bps for the broad market. As with HY, tech has therefore seen an isolated repricing, but absolute levels remain tight relative to history.

Despite the rapid development in AI and the elevated valuations across parts of the tech sector, it is important not to run ahead of ourselves. Several of the arguments in the article stem from misinterpreting system-wide infrastructure commitments as single-company borrowing plans, or from treating modest spread widening as evidence of funding stress. The reality is that we are in the midst of a large infrastructure cycle that is naturally financed through the bond market, and spreads remain tight relative to history despite the rise in supply. There are legitimate questions about how quickly this development can continue, but the credit market is behaving largely in line with historical precedent. For now, the data do not support the narrative of an imminent funding squeeze for the sector.

Merk: Å kjøpe og selge aksjer innebærer høy risiko fordi verdien i verdipapirer vil svinge med tilbud og etterspørsel. Historisk avkastning i aksjemarkedet er aldri noen garanti for framtidig avkastning. Framtidig avkastning vil blant annet avhenge av markedsutvikling, aksjeselskapets utvikling, din egen dyktighet, kostnader for kjøp og salg, samt skattemessige forhold.

Innholdet i denne artikkelen er ment verken som investeringsråd eller anbefalinger. Har du noen spørsmål om investeringer, bør du kontakte en finansrådgiver som kjenner deg og din situasjon.