Lesetid

8 min lesetid

Publisert

08. mar. 2021

Artikkelen er flere år gammel

This is where we stand.

During the last week of February, the EU Commission hosted a series of webinars on the EU Taxonomy together with the Platform on Sustainable Finance (the “Platform”), the expert group advising the Commission on the development of the Taxonomy.

The purpose of these webinars was to give a general update on progress and also to answer to some of the questions and misunderstandings that has circulated since the EU Commission published its draft delegated acts in November 2020. These drafts include technical screening criteria for the first two of the six environmental objectives – Climate Change Mitigation and Climate Change Adaptation.

The drafts spurred strong reactions in the market and the Commission received more than 47.000 responses during the public consultation phase which ended on December 18th. The initial plan of publishing the final delegated acts by year end was delayed, and during the February webinars the Commission communicated that the updated versions would be published in the second half of April. Implementation as we understand it is still planned for January 2022, with investors asked to report on the share of their holdings that are Taxonomy aligned, and in annual reports for 2021, companies covered by the Non-Financial Reporting Directive are also asked to report on the share of their turnover and investments that are aligned with the Taxonomy criteria.

According to the Platform, the responses covered some 1.800 individual topics, which could mainly be categorized in four types:

The Taxonomy currently only covers the first two environmental objectives, which are focused on climate change. Naturally, CO2 emissions has been a central part of identifying which sectors and activities to include under these objectives, and the current list is assumed to cover sectors that stand for around 94% of Europe’s CO2 emissions. In other words – the work has focused on those sectors that have the largest negative impact on these two environmental objectives today, and which therefore can make the largest positive contribution going forward.

Many sectors and activities are yet to be included. Activities may be added over time to the first two environmental objectives, but other activities may be more relevant when looking at the remaining four environmental objectives:

One of the Platform’s subgroups – the Technical Working Group (TWG) – is currently developing draft criteria for these four environmental objectives and these are meant to be published June 25th with a public consultation ending July 30th.

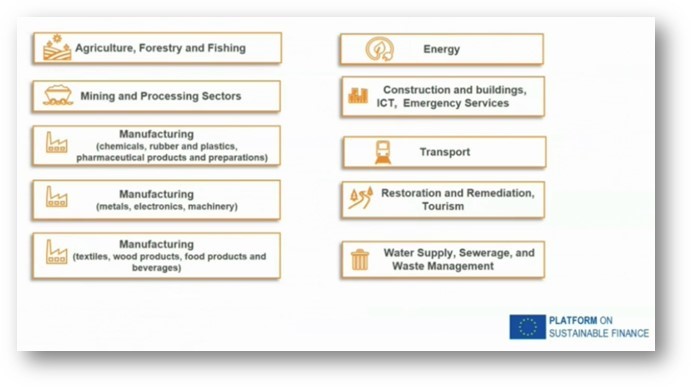

The TWG is currently working on criteria for the following sectors/groups (slide shown during webinar), but not all might be covered under all four environmental objectives. Again, inclusion depends on towards which environmental objective certain activities can be assumed to have the largest contribution.

There is a value chain approach from raw materials to waste management, and with a large focus on the manufacturing processes with three TWG sector teams focusing on developing criteria for various parts of the manufacturing industry.

Sustainable forestry was also mentioned as a topic currently in discussion. The proposed criteria for Forestry under the first environmental objective Climate Change Mitigation have been criticized by the industry for leaving Existing Forest Management out, and mainly focusing on Improved Forest Management. In short, this means that forestry operations today that do not lead to a significant improvement in carbon sinks for example could not qualify as Taxonomy-aligned. However, such forestry operations might be able to show significant contribution towards other environmental objectives. Among the possible overarching criteria for showing substantial contribution towards the sixth environmental objective Protection and restoration of biodiversity and ecosystems, the Platform listed “Sustainable forest management, including practices and uses of forests and forest land that contribute to enhancing biodiversity or to halting or preventing degradation of ecosystems, deforestation and habitat loss”.

It was also clarified that Fisheries will be included in the next round, however Aquaculture is not. There was no particular reasoning behind this choice other than resources and that the work will take place in steps with additional activities being included over time. Via Article 20 in the Taxonomy Regulation, proposals for relevant criteria for activities not yet covered can be sent to the Commission for review.

The Platform also highlighted that criteria are mainly developed based on what is feasible today, and what can be considered best available technologies. The Taxonomy aims to be technology neutral but updates will be made over time when technological developments mean that new alternatives become feasible. It will be the responsibility of the Platform to advise the Commission on when such updates should be evaluated.

One of the webinars also touched upon the possible extension of the Taxonomy to not only identify activities that can make a substantial contribution, but also to design a framework for activities making significant harm to environmental objectives. (In)famously referred to as a “brown Taxonomy”, this would in essence create three layers where activities either qualify as;

This could possibly answer to some of the criticism around the Taxonomy being too binary and provide a clearer distinction between harmful activities and those in transition. On the other hand, comments were also raised that elements of possible significant harm are already included in the current setup. For each activity, there will be substantial contribution (SC) criteria, and there will also be do no significant harm (DNSH) criteria. When quantitative thresholds are used, there may be a buffer between the SC and DNSH criteria levels, also identifying the “in between” layer of low or no contribution.

One of the webinars focused on the usability of the taxonomy and the current lack of data for investors to fulfil their reporting requirements. One of the Platform’s six sub groups is tasked with tackling these challenges and provide guidance. It was argued that much of the information needed to report is already available, but not structured in a way that makes it easily extractable for stakeholders, and it will take significant resources from companies to align their reporting with the Taxonomy reporting structure. However, once completed it will be easier going forward and also provide significant benefits to investors and other stakeholders with a harmonized set of data. Several data providers are also working to align their data offerings with the Taxonomy classifications and metrics needed to report. It was also highlighted by the sub group that it is expected that the first Taxonomy reporting from companies and investors will be a “trial and error” process that will improve over time. As much of the data will still be unavailable, it is understood that the first reporting will be based on estimations and proxies and reported on a “best intention basis”.

We daily receive questions on various aspects of the Taxonomy. Many of the concerns relate to what it means in practice to be Taxonomy-aligned, or perhaps even more so – what it means to be non-aligned. We think there have been varying views and also possible misunderstandings on this matter. As clarified by the Commission and the Platform during these webinars, the Taxonomy is not a list of what to do and what not to do. It is not a list of which assets investors and banks should or shouldn’t finance. Yes, the Taxonomy is binary, but that does not mean that an activity currently not living up to the criteria is deemed to be unsustainable or bad.

Europe has an ambitious agenda to become carbon neutral in 2050. The Taxonomy is one, but not the only, component of this work. The Taxonomy helps us to create a common language and reporting standard, but we can’t forget that this is a long term plan. First and foremost, the Taxonomy, and the surrounding regulations, imposes reporting requirements on financial market participants and companies.

Carbon neutrality will not happen overnight, but capital is needed to get there. Over time, we need to invest so that the share of Taxonomy-aligned assets increases, which means also investing in the transition.

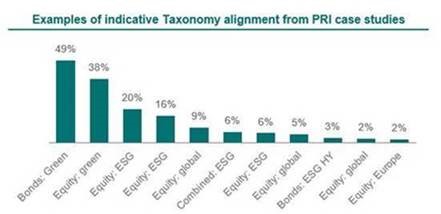

Looking at the current investible universe, we will most likely start off with a very small share of Taxonomy-alignment, but by steering capital both to Taxonomy-aligned activities, and activities promoting the transition, this share will grow over time. Various analysis have been published indicating that the share of Taxonomy alignment on a broader scale might be less than 5%. The below graph is a summary of EU Taxonomy alignment case studies that were published by various investors as part of a UN PRI project. The analyses were published a little over a year ago, which means they are not using the latest criteria proposals, but still provide valuable insights into what we can expect in terms of Taxonomy alignment. Each bar shows the indicated Taxonomy-alignment for a specific fund and the focus of each fund is indicated by its name in the graph.

These numbers also illustrate that for most investors and banks, it will not be feasible to only finance Taxonomy-aligned investments, although the aim will be to increase the share over time. It is also important to remember that the Taxonomy will not replace the ESG analyses that investors and banks are doing already today as part of their lending and investment decision processes.

In addition to being a reporting standard, the Taxonomy will also form the basis for other standards, such as the proposed EU Green Bond Standard. This is proposed to be a voluntary standard, based on current best practice and with the addition that use of proceeds should be Taxonomy-aligned. We will surely see a number of EU Green Bonds going forward, but we expect the current ICMA standard to dominate the market in the short to medium term as a result of the low share of Taxonomy-aligned assets.

To be continued…