Lesetid

10 min lesetid

Publisert

02. des. 2025

Artikkelen er flere år gammel

Credit markets update:

AI is increasingly described in superficial, binary terms as either a ‘bubble’ or a ‘breakthrough’.

Credit markets, however, are signalling something far more nuanced. This letter looks at what spreads are actually pricing, and at the parts of the financing structure that remain genuinely hard to assess.

First article: Should we worry about debt-funded AI infrastructure?

A few years ago, I wrote about decision-making and uncertainty, drawing on an example from Daniel Kahneman’s book Noise. Consider the following thought experiment:

When Julie was four years old, she had learned how to read.

What average grade do you think she achieved in her university years?

Most of us who receive only this short description will be inclined to think she did very well. We may not conclude that she was top of her class, but many of us will assume she performed above average – perhaps mostly As with some Bs. After all, early reading at the age of four is highly uncommon.

Let us add more context.

Julie was an only child. Her father, a highly recognised lawyer, was diagnosed with an autoimmune disease when she was three and began working from home. He spent much of his time with her and, with patience and care, taught her how to read. His attempts at teaching her arithmetic were less successful. In primary school she was a good, but not outstanding, student and not among the most popular. Her parents divorced when she was 11, after which she struggled more. In high school she did well in physics but cared less for several other subjects, finishing with an average grade of 4.5. She was not admitted to the top-ranking university she applied to and instead enrolled at a community college to study environmental sciences. Her first two years were characterised by emotional swings, including a period of smoking weed. By the end of her fourth semester, she straightened up and decided she wanted to pursue medicine. From that point on she took her studies far more seriously.

What average grade do you think Julie managed to achieve in her university years now?

The Julie example illustrates how easy it is to draw confident conclusions when we have too little information. When all we know is that she learned to read at the age of four, it is tempting to infer that she must have done well later in life. Early reading is often associated with talent or a supportive home environment, and from there we readily assume above-average academic performance. But this inference ignores everything we do not yet know. Once we add the missing pieces, the picture becomes more complex, and the conclusion far less obvious. More information did not give us a clearer answer; it made the question harder because we no longer had a simple model to lean on.

The current debate about a potential AI bubble follows a similar pattern. The headlines are simple, intuitive and decisive. After Nvidia reported its Q3 figures last week, Bloomberg wrote: “Nvidia’s upbeat forecast soothes fears of AI market bubble.”

The Wall Street Journal ran: “Nvidia’s strong results show AI fears are premature.”

The Financial Times added: “Nvidia shrugs off ‘AI bubble’ anxiety with bumper chip demand.”

What these headlines share is that they activate the “bubble” narrative even when the underlying message is positive. This primes readers to think about bubbles and nudges them to interpret new information through that lens. They also reinforce the impression that bubble concerns are widespread and legitimate. Terms such as “soothes fears”, “shrugs off anxiety”, and “fears are premature” imply that the fears exist and are significant enough to require a response.

The framing is binary: bubble versus no bubble. As an analyst, I encounter this constantly. People want a yes-or-no answer.

This is a problem because few of us have a strong intuition about bubbles. The last episode of some magnitude was the dot-com bubble 25 years ago. When intuition is weak, the safest response is to delay it. If you form an early view, you stop integrating new information. As Daniel Kahneman told Adam Grant in an interview, after that “you are just rationalising your own decision or confirming it.” This is a well-known trap in financial and economic research. Once forecasters adopt a view, they often pay more attention to data that confirms their hypothesis than data that contradicts it.

The way to avoid this is to remain undecided for as long as possible. As an investor, you should postpone major positional decisions. Don’t go underweight before you must. Instead of asking whether this is a bubble, you should ask what you need to understand about the current dynamic that increases or decreases the likelihood of one. For instance, if you worry about debt trajectories, you should examine the funding structures and speak to people who analyse credit markets daily. Anything else risks being superficial.

As I wrote last week, it is not my role to determine whether today’s AI dynamic is a bubble. Personally, I am deeply impressed by what OpenAI has achieved and see the potential for dramatic changes in how we organise work and societies. My own work life has already changed. At the same time, I know I am biased because I am comfortable with new technologies and tend to assume others have similar abilities. I also “know” Nvidia emotionally: I was a 14-year-old gamer who saved for a long time to buy the GeForce 256 SDR, the first consumer GPU. Nvidia was not just cool; it had a genuinely superior product. Gaming was never the same.

I will therefore refrain from discussing bubbles today as well. Instead, I will continue to dig deeper. Last week I touched on the use of debt in infrastructure cycles, and recent spread changes; since then, prices have moved further and deserve attention. And because many investors worry about circular financing, I will look at that too.

Before turning to circular financing, it is useful to look at what credit markets are actually signalling. Headlines about “AI bubbles” or “fragile debt dynamics” suggest broad stress, but spreads give us a more reliable picture of how investors are pricing risk. And here the story is far more nuanced.

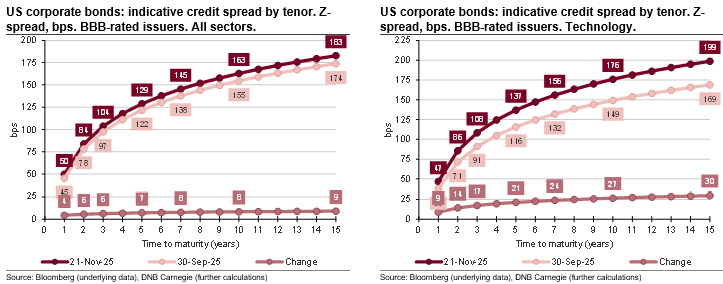

To begin with, the recent widening is not broad-based. In the BBB space – which dominates the US bond market – spreads have moved only modestly. From the end of Q3 to last Friday, BBB-sector spreads widened by less than 10bps, with 5-year indicative spreads now at 129bps.

In technology, spreads have widened somewhat more, though still not dramatically. 5-year indicative tech spreads have moved from 116bps to 137bps, while 10-year spreads are at 176bps, around 25bps wider than at the end of Q3. For comparison, industrial 5-year spreads are now at 116bps (up 6bps), and 10-year spreads have widened by 8bps to 145bps.

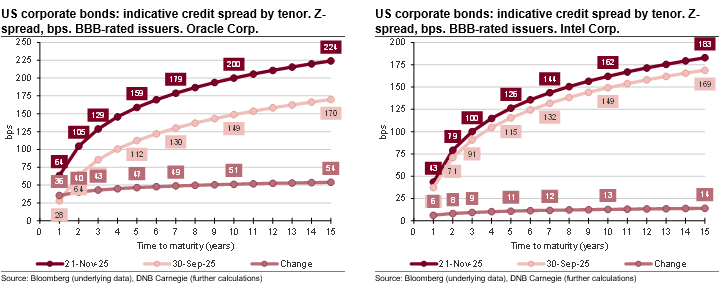

The widening within tech is also highly concentrated, driven mainly by Oracle. Its bonds have repriced by roughly 35–50bps since the end of Q3. Another large BBB-rated tech issuer, Intel, has seen only modest spread moves of 8–13bps across most maturities.

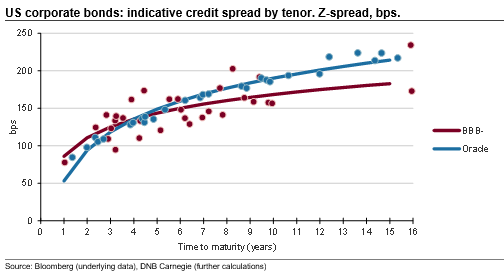

With these adjustments, parts of Oracle’s curve now trade more like a weak BBB-, especially at longer tenors, which screen cheap relative to other BBB tech debt.

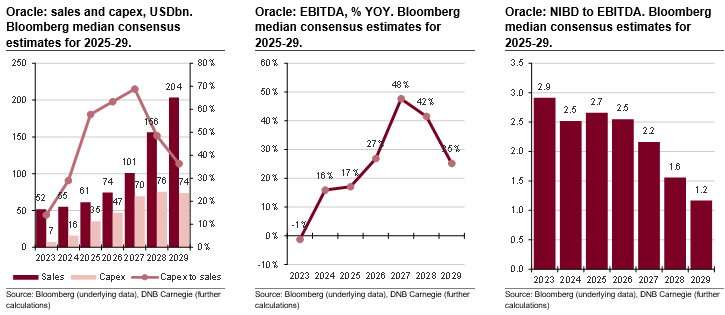

The market reaction to Oracle is understandable. The company is undertaking unusually large investments, with Bloomberg consensus estimating capex at 58% of sales this year and above 60% in the next two years. Consensus also expects this spending to drive earnings meaningfully higher, with EBITDA forecast to rise nearly 30% next year and 40–50% in the two years after that. If this materialises, leverage should gradually normalise from today’s elevated levels.

Naturally, markets are uncertain about Oracle’s ability to absorb a rapid debt build-up while delivering earnings growth at the pace analysts expect. But importantly, credit markets are not extrapolating Oracle’s risk to the broader sector. Large tech players such as Microsoft, Amazon, Meta and Alphabet, all of which are planning sizeable investments, continue to be viewed as fundamentally strong. All are either net cash or run with negligible net debt.

This differentiation is telling. Credit markets are not behaving as if there is a systemic problem or coordinated stress in the AI-related debt complex. They are doing the opposite: pricing company-specific risks in a measured way.

Is circular financing bad?

Having looked at spreads, it is worth turning to another concern that has gained traction in recent weeks: circular financing. Several commentators argue that a large portion of AI-related investment is being funded through arrangements where companies invest in, lend to, or contract with each other in ways that create interdependence. To assess this, we first need to clarify what the widely reported USD1400bn figure actually represents.

The key number here is OpenAI’s long-term ambition to secure roughly 30GW of compute capacity over the next eight years. Importantly, this is a strategy for long-term capital mobilisation, not a single binding purchase order on OpenAI’s current balance sheet. The figure aggregates the multi-year data-centre buildouts that Microsoft, Oracle, AWS, and others would need to undertake to satisfy the demand implied by OpenAI’s forward contracts and expected growth.

In practice, the structure looks like this:

This means the number reflects system-wide investment needs, not a financing obligation carried solely by OpenAI.

Large capital-intensive industries have relied on non-bank financing structures for decades. In the US corporate market, non-bank loans have historically been the second-largest source of credit after corporate bonds. Before 2010, this included:

GE Capital is a well-known example: for many years, customers financed GE equipment purchases directly through GE’s finance arm. Telecommunications equipment, aircraft engines, and industrial machinery have long relied on similar structures.

From this perspective, AI-related vendor financing sits within a long and established tradition of non-bank funding in capital-intensive sectors.

While AI financing shares similarities with historical vendor-finance models, it also differs in several important ways:

Product maturity. Traditional vendor financing supported proven, physical products with predictable revenue streams. AI infrastructure depends on demand for technologies that are still evolving and whose long-term adoption path is uncertain.

Buyer risk profile. Historically, the customer was an established industrial or telecom firm with a known credit history. In the AI case, the core buyer (OpenAI) is unprofitable and may remain so for some time.

Financing structure. In traditional models, the vendor provided a loan or lease to the customer. In AI, the structure is more intertwined: vendors may invest equity, provide financing, and rely on future off-take contracts, creating more interdependence.

Scale. AI infrastructure is being built at a scale far beyond traditional vendor financing. The combined capex across partners is an order of magnitude larger than typical historical examples.

Risk focus. Traditional vendor finance focused on the borrower’s ability to repay. In the AI case, risks relate more to technology adoption, timing, and the buyer’s ability to scale revenue fast enough to justify the investment.

The concern, therefore, is not that vendor financing exists – it has always existed. It is that this is vendor financing applied to an emerging technology, involving an unprofitable buyer, and executed at unprecedented scale. This is what makes the structure appear circular or fragile to some observers.

Summary

I want to end with a reminder of what this report is, and what it is not. It is not an attempt to determine whether the current AI cycle is a bubble. The main reason is simple: the underlying dynamics are far too complex for such a binary conclusion, and no single analyst has a full overview of the technological, commercial and behavioural forces involved. What I can do, however, is examine the parts of the puzzle where I have knowledge and competence, and where the data allow for more grounded assessments. These areas do not answer the bubble question, but they help clarify pieces of it.

On credit markets, the recent price moves appear orderly. The widening we have seen is modest overall, and where spreads have adjusted more meaningfully, notably in Oracle’s case, the moves look analytical rather than stress-driven. Markets are differentiating risk rather than extrapolating fear, and that is usually a healthy sign.

The picture is less conclusive when it comes to circular financing. Vendor financing has long been a feature of capital-intensive industries, but AI infrastructure differs in scale, maturity and the credit profile of the primary buyer. Whether this introduces fragility depends largely on adoption: if AI demand grows at the pace OpenAI and its partners assume, the model looks viable. If not, these structures could become more challenging. At this point, it is difficult and perhaps unwise to be definitive.

The broader point is that high-level narratives often obscure the underlying complexity. When headlines prime us to think in terms of bubbles, we naturally gravitate toward simple conclusions. But the dynamics here are anything but simple. Remaining undecided for as long as possible is not a weakness; it is an essential part of good analysis. My aim in this report has been to add depth where I can, and to highlight where uncertainty remains genuinely irreducible.

Merk: Å kjøpe og selge aksjer innebærer høy risiko fordi verdien i verdipapirer vil svinge med tilbud og etterspørsel. Historisk avkastning i aksjemarkedet er aldri noen garanti for framtidig avkastning. Framtidig avkastning vil blant annet avhenge av markedsutvikling, aksjeselskapets utvikling, din egen dyktighet, kostnader for kjøp og salg, samt skattemessige forhold.

Innholdet i denne artikkelen er ment verken som investeringsråd eller anbefalinger. Har du noen spørsmål om investeringer, bør du kontakte en finansrådgiver som kjenner deg og din situasjon.